Bitcoin VWAP Calculation on Multi Exchanges

This project provides a comprehensive solution for calculating the Volume Weighted Average Price (VWAP) of Bitcoin trades across multiple cryptocurrency exchanges. VWAP is a crucial metric in financial analysis, offering traders and analysts insights into the average price of an asset, weighted by trade volume, over a specific time interval. By integrating trade data from multiple exchanges and processing it with Python, this project delivers accurate, actionable results that can be applied in trading strategies and market analysis.

PYTHON-SCRIPTINGDATA VIZUALISATIONTIME SERIES

4/28/20241 min read

Main Features

VWAP Calculation

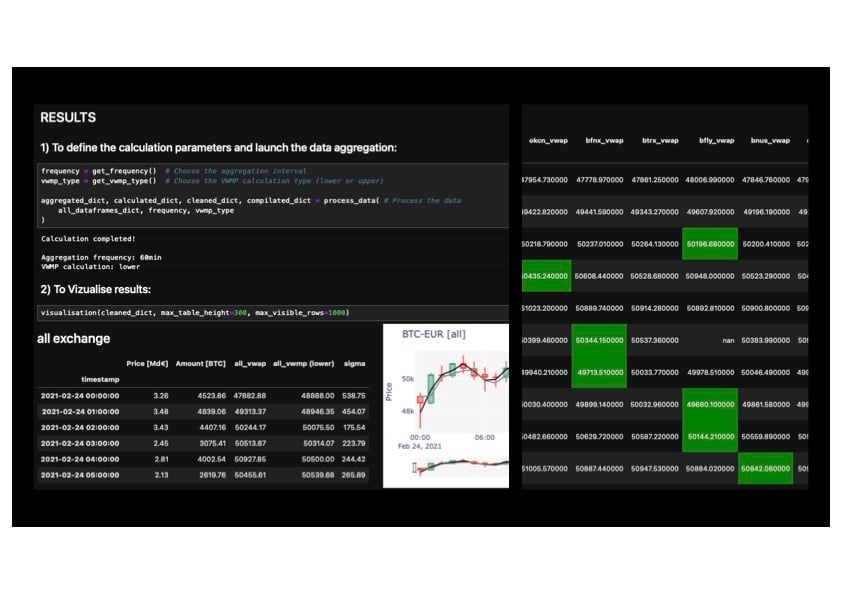

Computes VWAP for each exchange individually and for the global market, using hourly intervals.

Handling Missing Data

Identifies and addresses gaps or incomplete datasets to ensure accurate calculations.

Additional Metrics

Volume Weighted Median Price: A robust measure of average price with volume weighting.

Standard Deviation of VWAP: To assess volatility.

OHLC (Open, High, Low, Close): Summarizes price movements within each interval.

Flexible Time Intervals

While the default interval is hourly, calculations can be adapted to custom intervals like 5 or 30 minutes.

Output and Export

Exports results to CSV for seamless integration into reports or additional analyses.

Technology Stack

This project is implemented in Python, leveraging its robust ecosystem of libraries for data manipulation, numerical analysis, and visualization:

Core Libraries

pandas: For efficient data manipulation and aggregation.

numpy: For mathematical and numerical operations.

Visualization

plotly.graph_objects: For creating interactive and dynamic visualizations.

Utilities

datetime: For handling and transforming timestamps.

os: To facilitate file operations.

IPython.display: To enhance the interactivity of Jupyter Notebooks.

Project Workflow

Input Data

Trade data is loaded from CSV files, each containing columns for Timestamp, Price, and Volume.

Data Manipulation

The data is merged, timestamps are standardized, and it is grouped by hourly intervals for each exchange.

VWAP Calculation

VWAP is calculated for individual exchanges and globally, providing a consolidated view of market dynamics.

Output

Results are exported as a CSV file, indexed by hourly intervals, with columns representing VWAP values for each exchange and the global market.